Photo by TED Conference on Flickr

What’s the problem?

First the good news: extreme poverty halved between 1990 and 2010. This amazing fact shows what is possible. But still 1 in 10 people in the world live on less than $1.90 a day. In nearly 25 years, the average annual income of the poorest 10% of people in the world has risen by less than $3 and their daily income by less than a single cent each year.

Even the world’s wealthiest countries have pockets of extreme deprivation. In some of the poorest regions of the American south, such as Alabama, poor sanitation means people still suffer from intestinal parasites more commonly found in developing countries. In the US economy, a rising tide doesn’t lift all boats: instead, the poorest are sinking. In 2018, the UN’s special rapporteur on extreme poverty in the US found the poor were “becoming a more deprived and destitute class”. In the UK, the number of people dying from homelessness has more than doubled in the last five years.

And it’s clear that we could be going further and faster if it weren’t for our broken economic system.

What does that mean?

Finance has the potential to lift people out of poverty. But all too often our system does the opposite.

Since 2010, the poorest half of humanity have received only 1% of the total increase in global wealth. Their wealth has actually been falling – to the tune of around $1 trillion.

How does finance affect this?

By preying on the most vulnerable people and countries, our financial system encourages a cycle of poverty and debt:

- Through “vulture funds”

Perhaps the most notorious example of predatory finance profiting from poverty! The nickname ‘vulture funds’ refers to sophisticated hedge funds that buy up the debts owed by nearly bankrupt nations at knock-down prices, and then sue them aggressively for the full amount the debt was originally worth. Vulture funds target:

—- Debt-ridden countries: Back in 1999, one fund bought $30m of Zambia’s debt for just $3m, just as it was about to be cancelled by the Heavily Indebted Poor Countries (HIPC) initiative. They then sued Zambia for the full amount plus interest – $55m – and won. The fund gained 17 times the value it had invested; Zambia lost 15% of its social welfare budget, funds that could have been spent on alleviating poverty.

—- Developed countries: Argentina suffered a similar fate after its financial crisis in 2001. It ended up paying out $4.65bn after being dragged through the US courts for over a decade. Vulture funds also began circling over Greece after it ran into problems following the financial crisis, and more recently over Venezuela.

—- Poor individuals: In Ireland, vulture funds like Lone Star are also buying up the bad debts of ordinary people who defaulted on their mortgages during the crisis – raising concerns that these people could be pushed out of their homes. The EU is even promoting this solution as a way of getting bad debts off banks’ balance sheets.

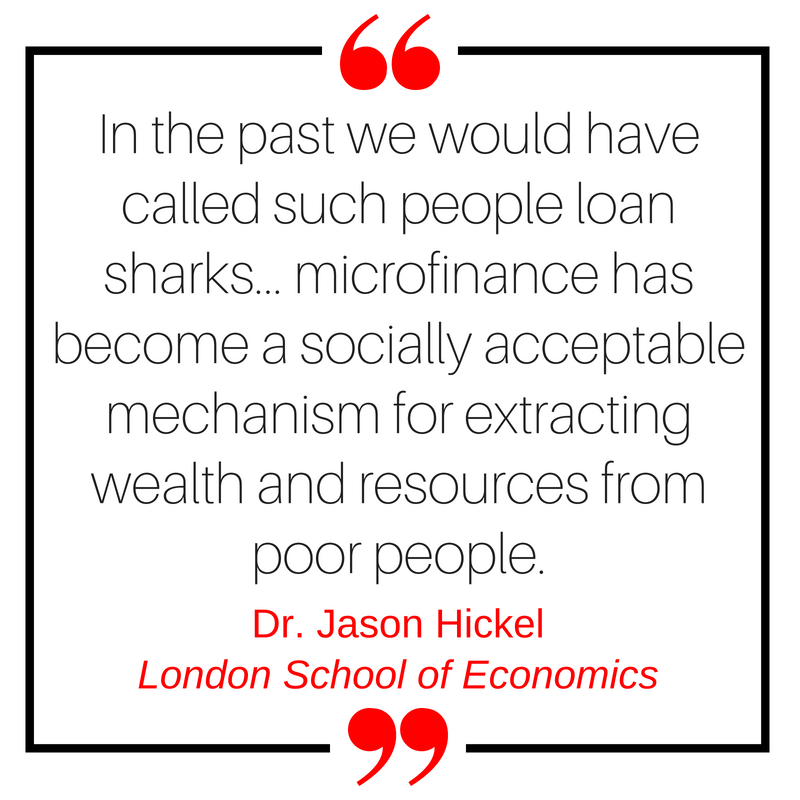

- Through microfinance

In the global south, small loans (or ‘microfinance’) have been championed for decades as the answer to poverty – but evidence shows they can make it worse. Most people don’t use them to start up businesses, but to pay for their basic needs, trapping them in a spiral of indebtedness. In South Africa, 94% of microfinance loans are used in this way. The real winners are the lenders, who often charge exorbitant rates of interest.

- Through legal loan sharks

Legal loan sharks target the poor in the global north as well. Having originated in the US, so-called “payday lending” – specifically targeted at people whose wages are not enough to make ends meet – have became a major industry in the UK. In a victory for citizen pressure, the regulator capped the cost of these loans in 2015. But lenders will surely move on again to other countries with lax regulation to prey on the poor. Meanwhile, loopholes in the cap mean that ‘doorstep lenders’ are still charging some UK borrowers eye-watering interest rates of up to 1,500%.

- Through expensive payment systems

It’s not just a few predatory lenders, but also the way finance and payment systems are designed. Migrant workers sending money home are hit with extra transfer fees, sometimes costing 12% or more, costing them 3.6 billion euros a year in Europe alone – more than the entire European emergency aid budget. Some groups, such as those experiencing homelessness, find it almost impossible to access the finance system at all – locking them out of the economy and trapping them in poverty. As digital payments replace cash, the finance system becomes even more powerful as the ‘gatekeeper’ to the economy. Exclusion from finance means exclusion from society.

- Through reckless global finance

Some of these crises were caused by reckless global finance in the first place. For example, even in countries with good credit ratings like the UK, austerity was introduced after the financial crisis. This was done on the grounds that it would keep bond markets happy – despite hurting the economy and leading to a new wave of stories like Donna’s.

In other words, our financial system plunges nations and individuals into poverty, and its most unscrupulous players then swoop in to profit from the resulting chaos.

How does this affect you?

Poverty is not an identity. As Donna’s story shows, any one of us could find ourselves experiencing poverty by an unlucky chance. And even if we are lucky enough to avoid this, as human beings we care about the poverty experienced by our neighbours, our friends, our families, and by children across the globe. In a world of abundance, nobody should be forced to go without food, shelter or healthcare. And when a financial system worth trillions of dollars is manufacturing poverty instead of preventing it, this is unacceptable. We must demand a finance system that works for people instead of profit.

What’s the way forward?

- FIGHTING INEQUALITY. Financial services should be designed and regulated to reduce their contribution to discrimination and inequality. Tax avoidance and secrecy havens are closed, debt relief is made possible for over-indebted countries. A fair taxation system redistributes wealth from the 1% to middle and working classes and from large corporations to the public purse.

- GOOD FINANCIAL SERVICES. Everyone should have access to basic, low-cost, transparent and un-exploitative financial services. Financial workers should be free to act in the best interests of customers.

- LESS PRIVATE DEBT. Society should be less dependent on the creation of private debt and money. Credit regulation should aim to prevent over-indebtedness and credit-fuelled speculative bubbles.

Our economic system is broken, but together, we have the tools to fix it. Join in.

Sources

World Bank, Poverty Overview

Oxfam, An Economy for the 1%

UN Human Rights Council, Report on Vulture Funds

FESSUD, Financialisation and Wellbeing

Also check out

FESSUD’s library of research on financialisation and wellbeing